Hello everyone. No surprise that we are publishing on Wednesday night this week. Has something to do with some activity that was centered around the DFW Metromess today. Yes, there were three American Airlines‘ union votes announced today — two passed and one didn’t. And the one that didn’t was the big one.

Hello everyone. No surprise that we are publishing on Wednesday night this week. Has something to do with some activity that was centered around the DFW Metromess today. Yes, there were three American Airlines‘ union votes announced today — two passed and one didn’t. And the one that didn’t was the big one.

The pilots at American Airlines decided that they would rather put their fate in the hands of U.S. Bankruptcy Judge Sean Lane than accept what many pilots apparently thought was an “unsatisfactory” contract.

As you can read in the blog post below, I thought the pilots should vote yes.

Meanwhile, the flight attendant voting period during which they need to decide if they are going to vote yes or no on their “last best and final offer” from the company continues.

As it is scheduled now, Judge Lane is supposed to rule on the airline’s request to abrogate the union contracts that have not been renegotiated next Wednesday as part of the standard Section 1113 procedure.

However, the outcome of the flight attendant vote will not be known by that time.

It will be up to the airline — whether it asks the judge to delay a ruling — or it simply allows him to abrogate the contracts that have not been agreed upon (which would then include the flight attendant contract) on Wednesday.

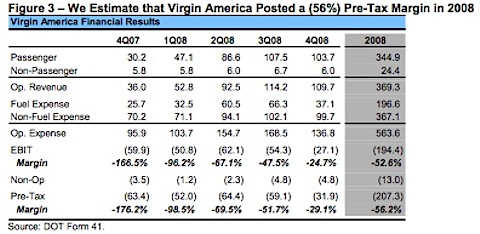

Meanwhile, this week is yet another big earnings week issue, as we take an in-depth look at the recent results of Spirit, Allegiant, Alaska Air Group, WestJet, and Republic Holdings.

We also give you overviews of the recent earnings news from IAG Group (owner of British Airways and Iberia), Virgin Atlantic, Lufthansa and Cathay Pacific.

Speaking of Allegiant, the airline said on its earnings call last week that it was very happy with the first month of its new service to Hawaii. The airline is using 757s to fly to Hawaii, and today, the airline announced even more service to Hawaii. Know what new routes were announced? Better yet, know which airline Allegiant seems to be targeting with their latest choices?

WestJet had an interesting announcement last week — for those of you who agree that passengers will pay for meaningful upgrades. The airline announced it was putting in four rows of “premium economy” seats on all of its 737s. It is also adding seats to its 737-800s.

Meanwhile, Spirit just keeps making money. Although I think the airline showed evidence of some growing pains in the second quarter — as costs were above where the airline wants them to be.

In terms of Republic Holdings, the hybrid holding company did quite well, as the Frontier Airlines’ restructuring process is really beginning to shine. So now what?

Meanwhile Republic continues to work through its issues with its Chautauqua, aka Chicken Taco, operation. Republic remains convinced it can make the 50 seat aircraft work –but it is going to have to be flown at exceptionally low rates to mainline airlines if that is the case.

While we don’t do a full earnings review of SkyWest this week, as they reported earnings today, I will tell you that the airline blew away estimates — sending shares of the stock up 23% on the day.

As always, all this, and more — in this week’s issue of PlaneBusiness Banter.

Also — a friendly reminder for our subscribers. This is our last issue for August. We are now officially on vacation. Our next issue will be published after Labor Day!