Monday the Bureau of Transportation Statistics of the DOT issued the latest Form 41 data for the industry. The information covered the fourth quarter 2008 numbers.

Needless to say, for airline geek types, the release of Form 41 data is like a huge box of goodies, all wrapped up with a nice big bow. The only problem is — you have to take the time to get in the box and carefully unwrap all the nuggets.

This morning analyst Gary Chase with Barclays issued a research note on Virgin America’s financial situation — a note that was clearly based on Gary and fellow analyst Dave Fintzen’s careful unwrapping of the Virgin America nuggets.

But wait — Gary doesn’t even cover Virgin America. The airline is not publicly traded.

Oh, but he does cover airlines that are currently affected by the airline’s presence. Most notably JetBlue and Alaska Air Group. Of all the major airlines Virgin overlaps about 25% of JetBlue’s capacity, while it overlaps about 17% of Alaska’s.

In his note this morning, Gary noted that while Virgin has been in the news a good deal lately because of questions concerning its ownership structure — “we cannot know the details of the company’s ownership structure.” But Gary and company can, and did, analyze the airline’s operating performance for the fourth quarter as reported to the DOT.

The verdict?

“The airline is now beyond the point in its development where JBLU turned profitable; Virgin America’s results would show losses in late 2008 even at sub-$1.00 fuel prices.

DOT filings point to substantial losses that go well beyond high fuel prices. We estimate that to break even in 2009 (similar to the rest of the industry on an un-hedged basis), the airline would need to drive significant improvement in revenue or cost performance, or both. For example, one path to break-even would be to achieve a roughly 20% higher unit passenger revenue (in an environment where industry RASM is declining by nearly 10%) and reduce non-fuel costs by almost 10% while fuel prices remain at the $1.49 level.”

He continued, “Virgin America’s premium strategy, including its First Class and Main Cabin Select products, does not appear to be generating a meaningful revenue premium. Rather, unit revenue performance lags JBLU and the industry at-large. Virgin America’s unit revenue performance has shown relative improvement as the airline spools-up, but still lags a typical new JBLU markets despite having a first class option and fewer seats on an equivalent aircraft (which should translate into both higher RASM and CASM). While Virgin America has found some relative success in short-haul West Coast markets, revenue performance in Transcon and longer-haul West Coast (i.e. Seattle) lags the industry by a wide margin.”

In addition, Gary said, “The premium strategy likely contributes to the airline’s relative cost problem, with non-fuel unit costs that are 40% higher than JBLU today and ~30% higher than JBLU at the same point in its life cycle. Unit cost tends to improve dramatically during the first year of an airline’s operations, but Virgin America is now beyond the point where JBLU’s cost structure stabilized. The cost structure remains significantly higher than JBLU, not to mention other low-fare airlines.”

In typical carefully worded “analyst-speak” he concludes: “We believe the Virgin situation represents a potential opportunity for the industry generally, but for JBLU and ALK in particular. Even if the press surrounding the ownership structure proves inaccurate, operating losses could also prompt a move away from its Transcon and long-haul West Coast routes, where performance has been the weakest.”

So how bad were the numbers themselves?

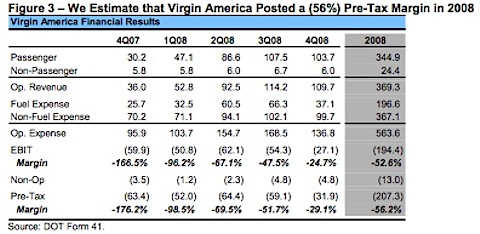

Virgin America’s recent DOT filings show the airline posted significant losses through its first year of operations. In total, the airline posted a 2008 pre-tax loss of ~$207mm on revenue of ~$370mm, for a pre-tax margin of negative 56%. While margins did improve, DOT reports show 4Q08 pre-tax margin was a negative 29% with a pre-tax loss of $32 million.

Now, is there anyone out there who still wonders why it was that Virgin America fought for so long to keep from reporting its results to the DOT?

I didn’t think so.